As land tax can be a significant expense for investment property owners, when considering a lease, it will be of interest for both the potential lessor and the tenant whether the land tax can be recovered from the tenant as an outgoing.

The following chart lists a simplified set of questions and outcomes for landlords and tenants to consider when looking at land tax.

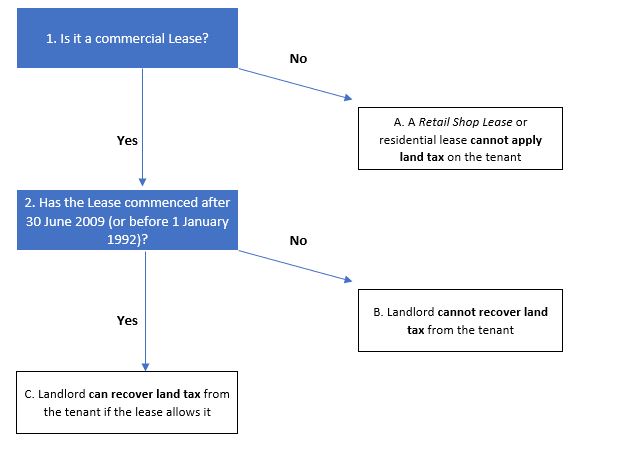

A. Residential or Retail Leases

Tenants in a retail shop lease cannot be required to provide land tax by the landlord. While landlord’s outgoings can be recovered in retail shop leases, clause 7(3) of the Retail Shop Leases Act 1994 (Qld), specifies that land tax cannot be included as a recoverable outgoing.

In residential leases, the Lessor must pay all charges, levies, premiums, rates or taxes for the premises, which includes council rates and land taxes, per clause 163 of the Residential Tenancies and Rooming Accommodating Act 2008 (Qld).

B. Leases that commenced between 1 January 1992 to 30 June 2009.

Commercial leases that commenced during the period between 1 January 1992 and 30 June 2009 cannot recover land tax from the tenants, even if there are provisions in the lease that allows for it.

However, per the decision in Vikpro Pty Ltd v Wyuna Court Pty Ltd [2016] QCA 225 in leases that commenced during this period, with land tax arising on or after 30 June 2010 which has: –

- already been paid by the tenant, then that amount can be retained by the landlord and the tenant cannot seek to recover the land tax already paid; or

- been ordered by the court to be payable by the tenant, that order can still be enforced.

- Leases after 30 June 2009

Since the decision in Vikpro Pty Ltd v Wyuna Court Pty Ltd and a legislative change in 2017, landlords in commercial leases that commence after 30 June 2009 will be able to recover land tax arising from 30 June 2010 onwards, as long as the lease permits it.

Potential tenants seeking to enter into a lease requiring contributions of outgoings, including land tax should ensure that they receive sufficient disclosures on the anticipated costs, including by seeking a land tax clearance search.

If you have any questions about a commercial lease and the recovery of land tax, please call us on (07) 3839 7555.