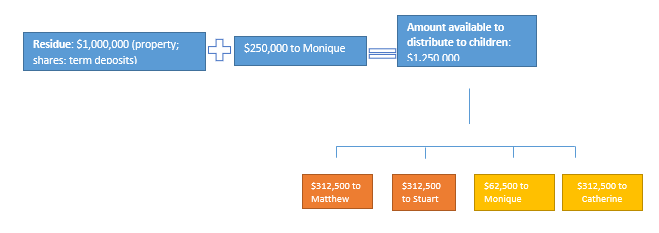

What do Trust deeds really do?

All trusts must have as a minimum, a Trustee, a beneficiary, Trust Property and the “Terms” of Trust on which the property (or asset) is held. This covers all types of trusts including “family trusts”, unit trusts in which each party holds a fixed interest in the income or capital and Self Managed Superannuation Funds, in which each member holds a “member benefits account” as a separate portion of the assets of the trust set aside for retirement. In each case the written terms of the trust are recorded in a signed document called a “Deed” by the person who settles the trust by providing the initial property of the trust (usually $ 10.00). The trustee accepts the appointment to act and the Principal or “Appointor” accepts the terms giving them the power to remove or appoint the Trustee. The precise wording of the deed is the basis for interpreting all of the powers of the trustee to distribute income and capital as well as how the trust will be managed, such as buying property or shares, selling, borrowing and final distributions at the end. The terms of the trust must be expressed with certainty and clarity, so the trustee knows to what extent they are authorised to do and the beneficiaries know when and how they can receive income or capital payments. It also governs what happens when you die and how you can allocate for tax purposes. If there are no clear rules then the ATO and any financial institution will use their position to limit what a trustee can do, often to the disadvantage of the beneficiaries.

Who keeps the trust deed and what if it is lost?

Usual practice requires at least three copies are created one for the client, one for the accountant and one for the legal advisor. This helps reduce the risk the original is lost. If no Deed can be located this creates difficulty in providing evidence of the terms of trust. If there is a dispute between beneficiaries, then this can cause major legal problems. A practical solution might be to locate a true copy of the deed and execute a new Deed of Confirmation to ensure there is a clear record of the terms. It is crucial to consider if an application to a Supreme Court to approve the terms is required so there is no doubt in the eyes of the Commissioner.

If there is no document on which to base a confirmation this will often lead to a dispute between family members. Often this is a major problem for estate planning and administration, because it is not clear who the successor in control of the trust assets should be. The question arises whether the assets held by the trust should fall back into the estate of the person who originally contributed to the trust or continue to be held on trust for a wider class of individuals. The legal costs of resolving these questions can be significant and the result very uncertain.

Practical Solutions

You must do absolutely everything possible to locate the Deed. Find out the details of any lawyer, accountant, property conveyancer or financial planner that ever advised the family. Very often we track down a person who has been incorrectly named as controller or “Appointor” and get them to sign a Deed of Amendment to rectify the control. The cheapest and easiest solution is to locate any copy of the signed Deed and any variations that have occurred since the start. It is sometimes possible to get clear evidence of the version of the Trust deed used by the advisor at that time and use that as a basis for an application to confirm the terms. Evidence for payment of the deed to date it and letters received at the time assist. It is of no help to just pretend the deed is not lost as eventually there will be a day on which a bank, a court or an estate will require it to be produced. Deal with the issue now while you are able to follow up all possible leads and sources so if a replacement deed is at all possible to be confirmed, then it is done at a time when there are no beneficiaries fighting over an estate. It is also a major issue when dealing with the tax office especially if you own shares in the trust and want to allocate franking credits between beneficiaries for tax purposes. If you cannot prove the power to do so by the trustee based on the trust terms the Commissioner will take a view about which beneficiary is deemed to receive what proportion of income on which they are taxed. The whole point of trusts is asset protection, the ability to invest collectively and the power to distribute in a way that saves tax. If you want a review of your trust deeds in the context of your estate plan please contact me at Tony.crilly@perspectivelaw.com or my direct line 07 3317 4312.